Advanced Capital Management Strategy:Modern Position Sizing & Risk Control 2025

Master professional capital management with Kelly Criterion, volatility-based sizing, portfolio heat management, and risk parity strategies used by institutional traders.

Table of Contents

What is Advanced Capital Management?

Advanced capital management is the sophisticated art and science of allocating trading capital to maximize returns while strictly controlling risk. Unlike basic position sizing that uses fixed percentages, advanced capital management dynamically adjusts position sizes based on multiple factors including market volatility, account performance, correlation between positions, and mathematical optimization models.

Professional traders understand that proper capital management is often more important than entry timing. A mediocre entry with excellent capital management will outperform a perfect entry with poor capital management over time. Advanced capital management transforms trading from gambling into a calculated business operation.

Key Components of Advanced Capital Management:

- Position Sizing: Determining the optimal trade size based on risk tolerance and account size

- Portfolio Heat Management: Controlling total risk exposure across all open positions

- Volatility Adjustment: Adjusting position sizes based on current market volatility (ATR-based)

- Correlation Management: Accounting for currency pair correlations to avoid overexposure

- Performance-Based Sizing: Dynamically adjusting sizes based on account performance and drawdowns

- Risk Parity: Allocating capital so each position contributes equal risk, not equal dollar amounts

- Drawdown Limits: Implementing strict rules to protect capital during losing streaks

The Evolution of Capital Management

Capital management strategies have evolved dramatically over the past three decades, moving from simple rules-of-thumb to sophisticated mathematical models used by hedge funds and institutional traders.

Traditional Era (1990s-2000s): Traders used simple fixed percentage rules like "never risk more than 2% per trade." While better than no risk management, this approach ignored market volatility, account performance, and position correlations.

Modern Era (2010s-2020s): Introduction of Kelly Criterion for optimal position sizing, volatility-based adjustments using ATR (Average True Range), and portfolio heat management. Traders began understanding that position sizes should adapt to market conditions.

Advanced Era (2020s-2025): Current state includes AI-powered dynamic sizing, risk parity strategies, correlation-adjusted position sizing, multi-timeframe capital management, and sophisticated risk-adjusted return metrics. Modern capital management is a complete system, not just a single rule.

Kelly Criterion Formula and Application

The Kelly Criterion is a mathematical formula that calculates the optimal percentage of capital to risk on each trade to maximize long-term growth. Developed by John Kelly in 1956, it's used by professional traders and hedge funds to determine position sizes.

Kelly Criterion Formula:

f* = (bp - q) / b

Where:

- f* = Optimal fraction of capital to risk

- b = Win-to-loss ratio (average win ÷ average loss)

- p = Win probability (win rate as decimal)

- q = Loss probability (1 - p)

Example Calculation: If your win rate is 60% (p = 0.60), average win is $200, and average loss is $100, then:

- b = $200 ÷ $100 = 2.0

- f* = (2.0 × 0.60 - 0.40) ÷ 2.0 = (1.2 - 0.4) ÷ 2.0 = 0.4 = 40%

⚠️ Full Kelly vs Half Kelly

Full Kelly (40% in example) is extremely aggressive and can lead to large drawdowns. Most professional traders use Half Kelly (20% in example) or even Quarter Kelly (10%) for more conservative risk management while still optimizing growth.

Fixed Fractional Position Sizing

Fixed fractional position sizing is the foundation of capital management. You risk a fixed percentage of your account balance on each trade, regardless of the trade setup. This ensures that as your account grows, position sizes increase proportionally, and as it shrinks, sizes decrease to protect capital.

How It Works: If you have a $100,000 account and use 2% risk per trade, you risk $2,000 per trade. If your account grows to $150,000, you now risk $3,000 per trade (still 2%). This creates a natural compounding effect.

Position Size Calculation:

Position Size = (Account Balance × Risk %) ÷ Stop Loss Distance (in pips)

For pip value calculation, use: Pip Value = Lot Size × Pip Size × Exchange Rate

Risk Percentage Guidelines:

- Conservative (1%): Suitable for beginners or during uncertain market conditions

- Moderate (2%): Standard for most professional traders, balances growth and protection

- Aggressive (3%): Only for experienced traders with proven strategies and emotional control

- Maximum (5%): Extremely risky, not recommended for most traders

Volatility-Based Position Sizing

Volatility-based position sizing adjusts trade sizes based on current market volatility, ensuring you maintain consistent risk regardless of whether markets are calm or volatile. This is crucial because a 50-pip stop loss in a low volatility environment represents different risk than the same 50-pip stop in high volatility.

Using ATR (Average True Range): ATR measures market volatility. When ATR is high, price moves more, so you need smaller position sizes to maintain the same dollar risk. When ATR is low, you can use larger positions.

Volatility Adjustment Formula:

Adjusted Position Size = Base Position × (Base ATR ÷ Current ATR)

Example: If your base ATR is 60 pips and current ATR is 120 pips (double volatility), your position size should be halved to maintain the same risk level.

Benefits: Volatility-based sizing prevents overexposure during volatile periods and allows optimal sizing during calm markets. This is especially important for pairs like GBP pairs and XAUUSD that have highly variable volatility.

Portfolio Heat Management

Portfolio Heat is the total risk exposure across all your open positions. It's calculated by summing the risk percentage of each open trade. This is critical because you can have multiple "safe" 2% positions open simultaneously, but if you have 5 positions at 2% each, your total portfolio heat is 10%—which is dangerous.

Portfolio Heat Zones:

- Green Zone (0-4%): Safe, conservative exposure. Ideal for most traders.

- Yellow Zone (4-8%): Moderate risk. Monitor closely and avoid adding new positions.

- Red Zone (8%+): Dangerous exposure. Close some positions or reduce sizes immediately.

⚠️ Maximum Portfolio Heat Rule

Never exceed 6-8% total portfolio heat. Professional traders typically keep it between 4-6% for optimal risk-reward balance. If heat exceeds 8%, you're one bad day away from significant account damage.

Correlation-Adjusted Position Sizing

Currency pairs are correlated—they move together or in opposite directions. EURUSD and GBPUSD have high positive correlation (around 0.85), meaning they typically move in the same direction. If you have positions in both, you're effectively doubling your risk, not diversifying.

How Correlation Affects Risk: Two 2% positions with 0.8 correlation don't equal 4% risk—they equal approximately 3.6% effective risk because the positions move together. You need to reduce position sizes when trading correlated pairs.

Correlation Adjustment Formula:

Adjusted Size = Base Size × (1 - Correlation Factor)

Example: If EURUSD-GBPUSD correlation is 0.85, and you want 2% risk on each, adjust to: 2% × (1 - 0.85) = 2% × 0.15 = 0.3% per position, or simply reduce each to 1% for practical purposes.

Common Correlations: EURUSD-GBPUSD (0.85), USDJPY-XAUUSD (-0.60 negative), EURUSD-USDJPY (-0.70 negative). Always check current correlations as they change over time.

Risk Parity Strategy

Risk Parity allocates capital so each position contributes equal risk, not equal dollar amounts. This is superior to equal dollar allocation because different currency pairs have different volatilities. XAUUSD (gold) is much more volatile than EURUSD, so equal dollar amounts create unequal risk.

Example: With $100,000 account and 5 positions at 1.5% risk each:

- EURUSD (low volatility): $15,000 position = 1.5% risk

- XAUUSD (high volatility): $8,000 position = 1.5% risk

- USDJPY (medium volatility): $12,000 position = 1.5% risk

Each position contributes exactly 1.5% risk, creating true portfolio balance. This is how hedge funds and institutional traders manage capital.

Dynamic Position Sizing Based on Performance

Dynamic position sizing adjusts trade sizes based on account performance. During winning streaks, you can slightly increase sizes (within limits). During drawdowns, you must reduce sizes to protect capital. This creates a natural defense mechanism.

Performance-Based Rules:

- After 10% account gain: Increase base risk from 2% to 2.2% (10% increase, capped)

- After 5% drawdown: Reduce base risk from 2% to 1.5% (25% reduction)

- After 10% drawdown: Reduce base risk to 1% (50% reduction), review strategy

- After 15% drawdown: Stop trading, reassess entire approach

This creates a "ratchet effect"—sizes can increase with success but must decrease with losses, protecting your capital during difficult periods.

Maximum Drawdown Limits and Recovery

Drawdowns are inevitable in trading. The key is managing them with strict limits and recovery plans. Drawdown recovery is asymmetric—a 10% loss requires an 11.1% gain to recover, a 20% loss requires 25% gain, and a 50% loss requires 100% gain.

Drawdown Action Plan:

5% Drawdown (Yellow Zone)

Reduce position sizes by 25%, review recent trades, tighten stop losses

10% Drawdown (Orange Zone)

Reduce position sizes by 50%, pause new trades, comprehensive strategy review

15% Drawdown (Red Zone)

Stop trading immediately, reassess entire approach, consider professional help

Recovery Math: Understanding that recovery becomes exponentially harder helps enforce discipline. A 15% drawdown requires 17.6% gain to recover. This mathematical reality should prevent over-leveraging.

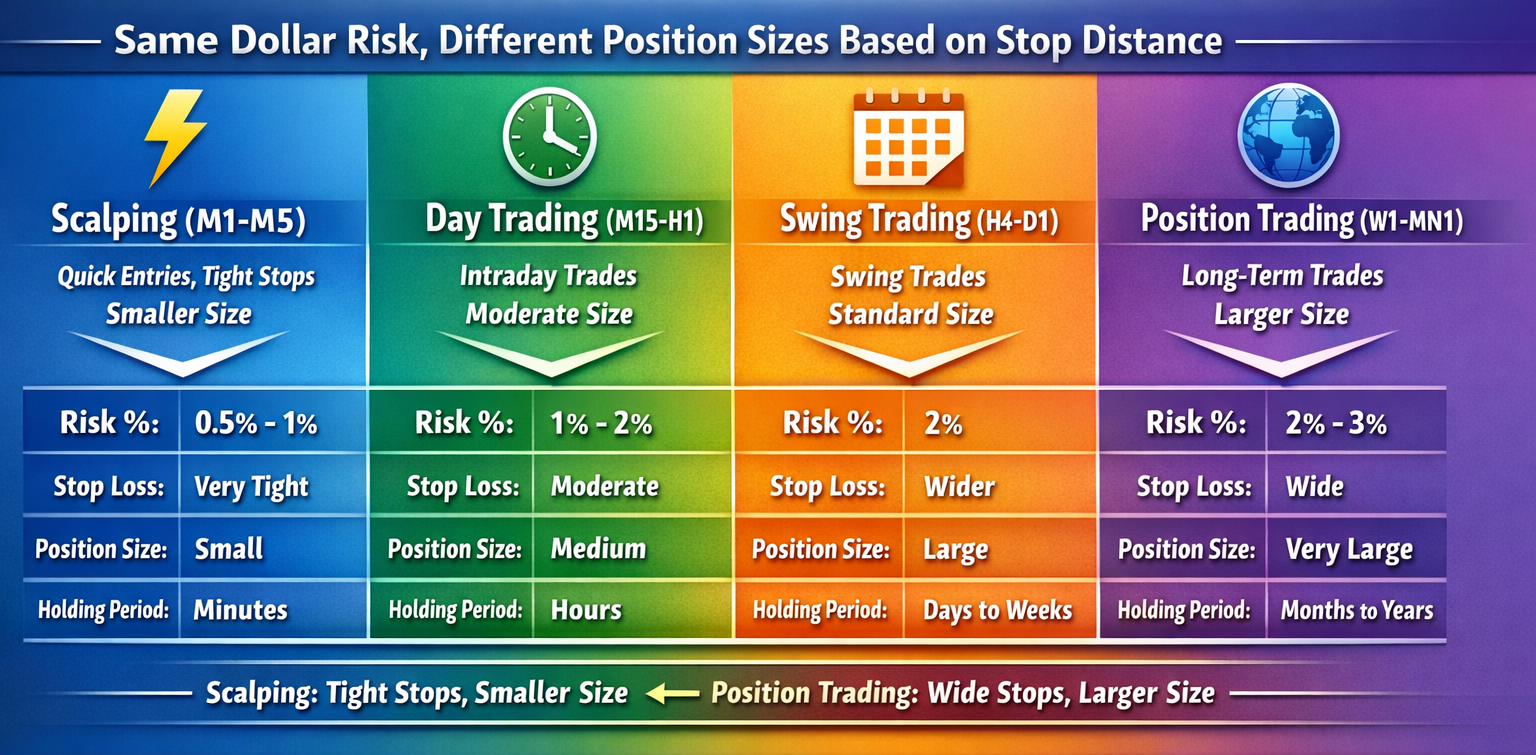

Multi-Timeframe Position Sizing

Position sizing should vary based on your trading timeframe. Scalpers need smaller positions with tight stops, while position traders can use larger sizes with wider stops. The key is maintaining consistent dollar risk across timeframes.

Timeframe Guidelines:

- Scalping (M1-M5): 0.5-1% risk, tight 10-20 pip stops, quick entries/exits

- Day Trading (M15-H1): 1-2% risk, moderate 30-50 pip stops

- Swing Trading (H4-D1): 2% risk standard, 50-100 pip stops

- Position Trading (W1-MN1): 2-3% risk, wide 100-200+ pip stops

The same $2,000 risk (2% of $100K) can be 2.0 lots on EURUSD with a 10-pip scalping stop, or 0.2 lots with a 100-pip swing trading stop. Same dollar risk, different position sizes based on stop distance.

Risk-Adjusted Return Metrics

Raw returns don't tell the full story. A 30% return with high volatility and 20% drawdowns is inferior to a 20% return with low volatility and 5% drawdowns. Risk-adjusted metrics reveal true performance quality.

Key Metrics:

- Sharpe Ratio: Measures return per unit of risk. Above 1.5 is good, above 2.0 is excellent

- Sortino Ratio: Like Sharpe but only considers downside volatility. Focuses on harmful volatility

- Calmar Ratio: Annual return ÷ maximum drawdown. Above 2.0 indicates good risk management

- Win Rate: Percentage of winning trades. 50%+ is good, but risk-reward matters more

Professional traders track these metrics monthly to ensure their capital management is working. If Sharpe Ratio declines, it's time to review position sizing and risk controls.

Capital Management Rules Summary

Here are the essential capital management rules that every professional trader follows:

- Never risk more than 2% per trade (1% for beginners, 3% maximum for experts)

- Maximum 6-8% portfolio heat across all open positions

- Use Kelly Criterion or Half-Kelly for optimal position sizing

- Adjust for volatility using ATR-based position sizing

- Account for correlations when trading multiple pairs

- Reduce size during drawdowns by 25% at 5%, 50% at 10%

- Maintain minimum 1:2 risk-reward ratio on all trades

- Stop trading at 15% drawdown and reassess strategy

- Review and adjust monthly based on performance metrics

- Track risk-adjusted returns (Sharpe, Sortino, Calmar ratios)

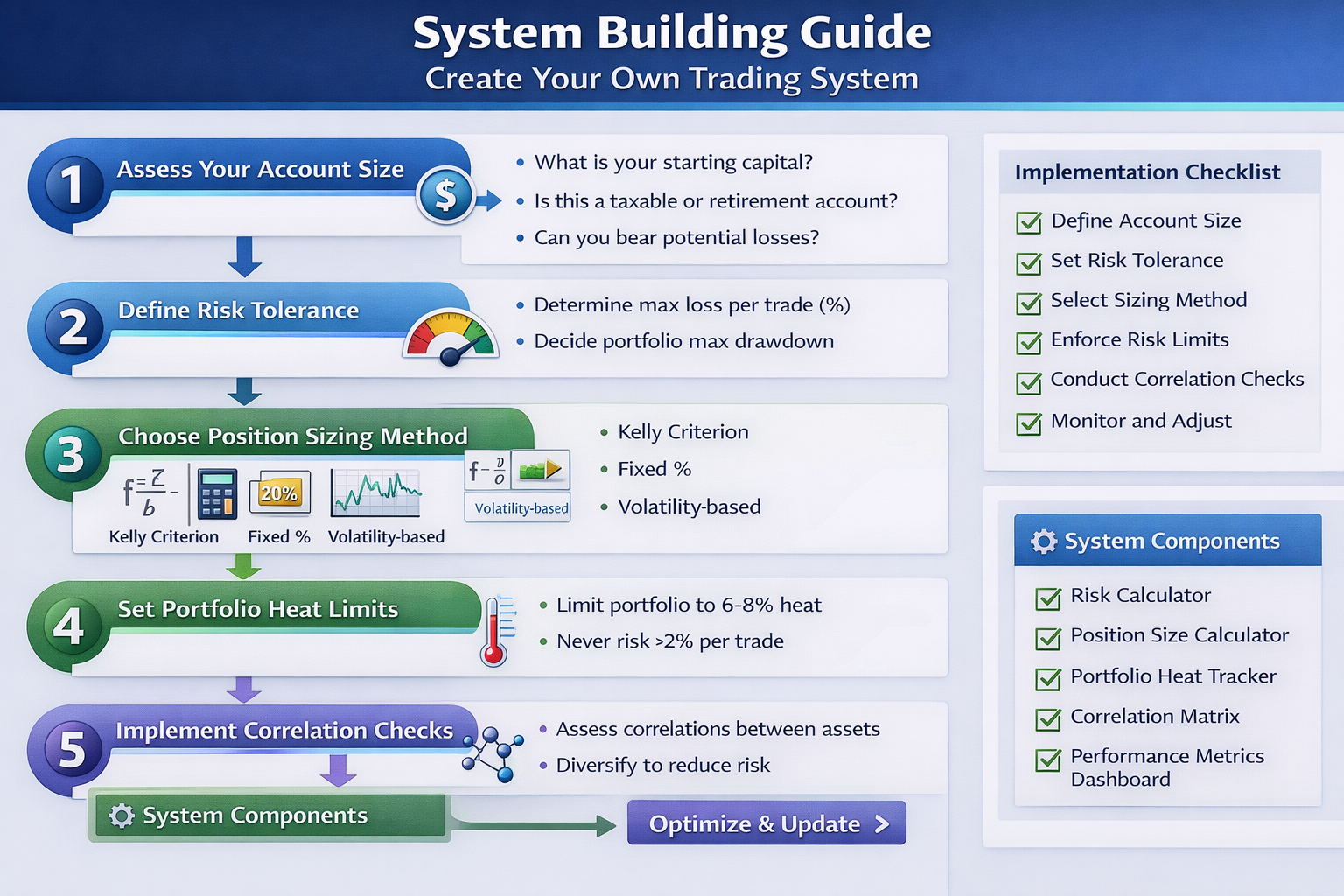

Building Your Capital Management System

Building a complete capital management system requires systematic implementation. Follow these steps:

- Assess Your Account Size: Determine your starting capital and risk tolerance. Smaller accounts (<$10K) should use 1% risk, larger accounts can use 2%.

- Define Risk Tolerance: Are you conservative (1%), moderate (2%), or aggressive (3%)? Be honest about your emotional capacity for drawdowns.

- Choose Position Sizing Method: Start with fixed fractional (2%), then add Kelly Criterion or volatility-based adjustments as you advance.

- Set Portfolio Heat Limits: Maximum 6-8% total exposure. Use a spreadsheet or trading journal to track this daily.

- Implement Correlation Checks: Before opening a new position, check correlations with existing positions. Avoid highly correlated pairs simultaneously.

- Monitor and Adjust: Review performance monthly. Track Sharpe Ratio, drawdowns, and portfolio heat. Adjust rules based on results.

System Components Needed: Risk calculator, position size calculator, portfolio heat tracker, correlation matrix, performance metrics dashboard. Many trading platforms include these tools, or you can use Excel/Google Sheets.

Related Articles

Risk & Position Sizing Primer

Master the fundamentals of risk management and position sizing to protect your capital.

Read ArticleTrading Psychology

Learn how psychology affects trading decisions and capital management discipline.

Read ArticlePut This Knowledge Into Action

Explore SignalWavesAI tools and start applying what you've learned with professional forex signals.